My Wednesday Wish for You: To Be Your Own Best Friend We often push ourselves harder than anyone else ever…

Read why you shouldn’t let headlines alone be your source of information.

Truth be told, headlines are a poor planning tool for anything. Even the major news organizations don’t get it right, certainly not all the time. They quote famous names, sell their product, and all too often emotions are formed, impressions develop, and decisions are made. What follows is a concise list of headline news from a period most will never forget.

Don’t Count on Headlines to Inform About the Future

•George Soros says US banks “basically insolvent” – Reuters, April 6,2009

• The financial sector ETF (XLF) established a monthly low in February 2009

• Warren Buffett: US Economy in “Shambles” With No Sign of Recovery – CNBC, June 24, 2009

• US Total Industrial Production’s low occurred in April 2009; the GDP low was in 2Q09.

• Debt crisis unsettles European economy – The Washington Post, February 6, 2010

• European Union GDP declined for one quarter (1Q10) before resuming its ascent.

• Dow’s Brief Fall of 1000 Points Sets Off Anxiety – The New York Times, May 6, 2010

• The S&P 500 declined further, hitting a monthly low in June, then closed up 28.1% one year later.

These headlines are from credible sources and quote credible people, but they are not looking at leading indicators and consumer trends and the host of other factors we look at every day at ITR Economics.

Reality Is Frequently More Nuanced Than the Headlines Have Room For

As we write this, the S&P 500 is officially back in bear territory. The market has been volatile, and S&P 500 decline makes people fear the future because of a perceived “wealth effect.”

The following is ITR Economics’ mid-June analysis. We do not have a snappy headline about hurricanes. Perhaps our headline would be “It’s Too Late to Get Out Now,” or “You don’t have to Rise and Decline With the Overall Market.”

• The stock market pain is concentrated primarily in the riskier sectors, like Technology.

• Energy is up double digits year-to-date, while several defensive sectors (Utilities, Consumer Staples) are hovering right around correction territory; Healthcare is in correction territory.

• We are at risk of further overall market weakness – particularly within Tech and tech-like stocks – for at least the remainder of June and likely through the summer as well.

• The weakness is likely to fade beginning late this year or early next year, and when it does the onset of recovery will come quickly, punishing those who exited the market recently or are thinking about doing so now.

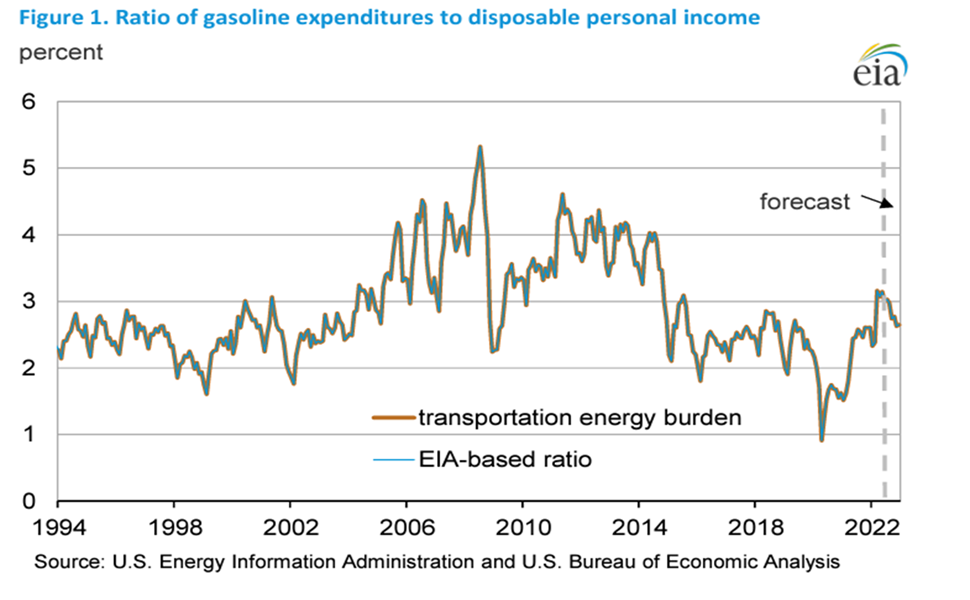

Have You Heard That Higher Gasoline Prices Will Torpedo Retail Sales?

That would be tough to prove based on data; however, it is often propagated as a truth, so people perceive it as a truth. According to the US Energy Information Administration and the Bureau of Economic Analysis, the ratio of gasoline expenditures to after-tax income in the US averaged 2.6% in the first quarter of 2022. The chart shows that we have certainly seen that ratio higher, and lower, in the past. The swing in the ratio is not consistently associated with good times or bad and is not well-correlated to the trend in retail sales (adjusted for inflation).

Our analysis shows that higher gasoline and diesel prices do not choke off retail sales. In fact, retail sales can keep moving higher at a steady pace even as gasoline prices move higher. That sounds counterintuitive, but it is reality. We complain about the price at the pump, but history shows that today’s prices are not likely to bring on a consumer-led recession.

Related Posts