When Ranjay Gulati, professor of business administration at Harvard Business School, began working on his latest book, he initially planned to call it Purpose. But he quickly realized he needed a new working title: During his research and writing process, he found that many companies like to talk about purpose but few back it up with their actions. For those few successful companies that did walk the walk, “it wasn’t just a purpose statement. It was a way of being. It was something that informed everything they did,” says Gulati.

That’s an important distinction, and it explains why Gulati ultimately titled the book, Deep Purpose. At Inc.’s virtual Purpose Power Summit Tuesday, Scott Goodson, founder and CEO of StrawberryFrog, spoke with Gulati about the idea behind his new book.

In its most basic form, Gulati says, a company’s purpose is a generalized intention about how you want to be in the world. A deeper, thoughtful purpose helps leaders set and achieve goals, not to mention go after a long-term vision. In other words, purpose is a key part of unlocking your company’s growth.

But how? For Gulati, the answer is multifaceted.

1. Your people are more motivated.

A deep purpose will help you attract and keep employees who are aligned with your company’s mission, and it will make them more productive. According to a 2015 Harvard Business Review study, inspired workers are twice as productive as satisfied workers. “When they [employees] connect their purpose with the company purpose, you get a different kind of person showing up,” Gulati says.

2. Your customers feel a greater connection to your brand.

More than ever, customers care about companies with purpose. They want their purchases to back brands that play a positive role in the communities in which they operate. The more you can connect with customers on the level of purpose, the more trust and loyalty you build.

3. Your business transitions from transactional to relational.

Partnerships, suppliers, customers, employees: Running a company today involves a lot of moving parts and lots of relationships. Think of this as your company’s ecosystem. Gulati says that having a deep purpose builds stronger relationships, which in turn strengthens your ecosystem. He says this transition will look like a “changing of a firm from an economic vision of a nexus of contracts,” where everyone is looking for their piece of the pie, to a “nexus of commitments,” where everyone is working toward that deep purpose.

4. You’ll always have a true north to guide your next moves.

Gulati says, “Purpose is a compass.” The ups and downs of running a business can be brutal, but a deep purpose will keep you on track no matter what challenges you face.

Finally, Gulati says, for leaders, a well-developed purpose helps them be more than just operators–they become inspirers. And that goes for not only inspiring employees in their day-to-day tasks but also inspiring them to work toward their own deeper purpose. That’s how leaders cultivate and grow their teams while also building a purpose-driven company from the ground up. Borrowing from Stanford University professor emeritus James G. March, Gulati says the world needs “leaders as both plumbers and poets.”

The traits of successful entrepreneurs haven’t changed much in the digital age: You need more builders than branders, and it’s key to have a technologist as part of — or near — the founding team. As a professor, I study businesses, and as an entrepreneur, I’ve launched several. So, I’ve come up with 4 essential questions that you should ask yourself if you’re seriously considering going out on your own:

Question 1: Can you sign the front, and not the back, of checks?

I know people who have all the skills to build great businesses, but they’ll never do so. Why? Because they could never go to work — after putting in 80-hour weeks — and write their own firm a check instead of receiving a check for their efforts.

Unless you’ve previously built firms and shepherded them through to successful exits or you know you have access to seed capital, you’ll need to pay your own company for the right to work your ass off until you can raise money. And most startups never raise the necessary money. Most people can’t wrap their heads around the notion of working without getting paid — and 99+ percent will never risk their own capital for the sheer pleasure of … working.

Question 2: Are you comfortable with public failure?

Most failures are private: you decide law school isn’t for you (because you bombed the LSAT), you decide to spend more time with your kids (you were fired), or you decide to work on “projects” (you can’t get a job).

However, there’s no hiding your own business failure. It’s you, and if you’re so awesome, your business must succeed … right? Wrong. And when it doesn’t, it will feel like elementary school, where the marketplace is a 6th grader laughing at you because you’ve wet your pants … multiplied by 100.

Question 3: Do you like to sell?

The word “entrepreneur” is a synonym for “salesperson.” Selling people to join your firm, selling them to stay at your firm, selling investors, and, oh yeah, selling customers. It doesn’t matter if you’re running the corner store or Pinterest — you’d better be darn good at selling if you plan to start a business.

Selling is calling people who don’t want to hear from you, pretending to like them, getting treated poorly, and then calling them again. I likely won’t start another business because my ego is getting too big to sell. I, incorrectly, believe our collective genius at my current business, L2, should mean that the product sells itself. Sometimes, it does. Entrepreneurship is a sales job with negative commissions until you raise capital, become profitable, or go out of business — whichever comes first.

The good news: If you like to sell and you’re good at it, you’ll always make more money — relative to how hard you work — than any of your colleagues, and they’ll hate you for it.

Question 4: How risk aggressive are you?

Being successful in a big firm isn’t easy, and it requires a unique skill set. You have to play nice with others, suffer injustices and bulls–t at every turn, and be politically savvy to get noticed by key stakeholders and garner executive-level sponsorship. However, if you’re good at working at a big firm, then, on a risk-adjusted basis, you are better off doing just that — and not struggling against the long odds that small firms face. For me, entrepreneurship was a survival mechanism, as I didn’t have the skills to be successful in the greatest platforms for economic success in history: big US companies.

With the endless and well-publicized stories of billionaire college dropouts, we romanticize entrepreneurship. But before you step into the cage of chaos monkeys, ask yourself and some people you trust the preceding questions about your personality and skills.

Taylor Swift has earned a lot of accolades. She has a dozen Grammy Awards, a Primetime Emmy, and a few hundred awards I’d never even heard of. She also managed to record and release two full-length albums in the second half of 2020. You remember 2020, right? You know, the year when finding a store with toilet paper in stock was an accomplishment.

On Wednesday, she added one more. New York University awarded her an honorary doctorate. At the commencement ceremony, Swift gave a 20-minute address to the graduating class, during which she shared what she called life-hacks.

Billboard magazine shared a transcript of the entire speech, and it’s definitely worth the read. Commencement speeches–especially the ones given by celebrity guests–are often dull and full of platitudes and cliche advice about how this group of graduates is going to change the world. Swift, on the other hand, is as gifted with words as anyone and uses them in a way that makes her relatable to just about everyone.

That’s why, even if you don’t have time to read the entire thing, you shouldn’t miss this section, right there in the middle:

I became a young adult while being fed the message that if I didn’t make any mistakes, all the children of America would grow up to be perfect angels. However, if I did slip up, the entire earth would fall off its axis and it would be entirely my fault and I would go to pop star jail forever and ever. It was all centered around the idea that mistakes equal failure and ultimately, the loss of any chance at a happy or rewarding life.

This has not been my experience. My experience has been that my mistakes led to the best things in my life.

We should pause for a second because most of us have no idea what the pressure must be like for someone who has lived almost all her life with the type of public exposure Swift has had. She talked in her speech about all sorts of circumstances that would make anyone want to give up. She shared about disappointment, loneliness, and the cost of making mistakes.

The thing is, if we’re really honest, we can relate. I mean, sure, there are plenty of things about being a teen country music star that are completely unrelatable for most of us. But, we all do dumb things. We mess up and break things. We hurt people, we make bad decisions, we take risks, and sometimes we fail. Or, so it seems.

Swift’s point is that mistakes don’t equal failure. And, if they do, it’s only because we let them. On the other hand, mistakes are often how we learn to succeed. It’s how we discover the boundary of our capabilities, and how we find ways to push even further.

The key is–and this is important–that Swift made a choice. Following the path from your mistakes to the best things in your life is a choice.

That might be the thing you need to hear: The key isn’t perfection, it’s whatever the next step is for you. And, if you make a wrong step–if you put your foot in the wrong place–you pick it up and take another. And another.

Eventually, you figure out your way. Eventually, your idea becomes real. Eventually, you make the thing and it works.

But, only if you don’t become consumed by your mistakes. When that happens, you stop trusting yourself to know where to put your foot so you stop taking steps altogether. Instead, learn from your mistakes–or, better yet, find someone else who has made them before you and is willing to help you. As Swift said:

Every choice you make leads to the next choice, which leads to the next, and I know it’s hard to know sometimes which path to take. There will be times in life when you need to stand up for yourself. Times when the right thing is to back down and apologize. Times when the right thing is to fight, times when the right thing is to turn and run. Times to hold on with all you have and times to let go with grace. Sometimes the right thing to do is to throw out the old schools of thought in the name of progress and reform. Sometimes the right thing to do is to listen to the wisdom of those who have come before us. How will you know what the right choice is in these crucial moments? You won’t.

That’s OK. Chances are, you’ll make a few mistakes. And those just might become the best parts of your life.

No, you aren’t imagining it: workers are leaving your company faster than you can replace them. According to the US Bureau of Labor Statistics, more than 4.3 million people voluntarily quit their jobs in December 2021, slightly below a record high in November 2021.

Their departures have left a huge hole in the labor market. The number of current job openings (10.9 million) exceeds the number of new hires (6.3 million). And in our own recent survey of almost 600 workers who voluntarily left a job without another in hand, 44 percent said that they have little to no interest in returning to traditional jobs in the next six months.1

In the past, spikes in voluntary attrition often signaled a competition for talent, where in-demand workers left one job for a similar but better one at another company. This most recent wave of attrition is different. Most are leaving to take on very different roles—or just leaving the workforce entirely. They have been operating under extreme circumstances for extended periods and have been unable to find an adequate balance between work and life—so they are choosing “life” until they absolutely need to go back.

The competition for talent is different now, too. Employers are competing with the full array of work experiences available to today’s employees—traditional and nontraditional jobs and, in some instances, not working at all.2 To get in the game, companies must offer adequate compensation and benefits packages; that is the ante. But to win, they must recognize how the rules of the game have changed. While workers are demanding (and receiving) higher compensation, many of them also want more flexibility, community, and an inclusive culture (what we call relational factors) to accept a full-time job at a traditional employer.

Traditional employers must compete across all these elements. They will likely need to adopt entirely new tactics to find and attract “latent” talent—workers who aren’t currently looking to rejoin the labor market but who might come back if they get the right offer.

In this article, we look at the employees who left a job without another in hand, who returned and why, and how companies can begin to bring more workers back into the fold. Now more than ever, companies must redefine their attraction and retention strategies and build a value proposition that takes employees’ whole lives into account. The longer they wait, the more burnout they will create among existing employees, potentially leading to even more attrition.

Among those who quit, attrition was most apparent in the consumer and retail, healthcare, and education sectors—industries that have felt some of the greatest social and economic pressures during the pandemic.

Why are employees leaving?

Because they can. Leaving a job used to be anxiety inducing; it isn’t anymore. The cost of switching jobs has gone down significantly. There is much less of a stigma associated with showing a gap in your résumé. Because of the current labor shortage and the greater acceptance of remote work, employees in many industries are confident that they can find work anywhere, whenever they are ready. They have access to more information about the labor market than ever before—through word of mouth and social-media sites, for instance—so they don’t need to rely on the usual recruiting resources. They have seen friends and colleagues depart and survive, and they are confident that they can, too.

Because they are upset.Those who voluntarily left cited experiences with uncaring leaders, unsustainable expectations of work performance, and lack of career advancement as factors in their decision (Exhibit 1). Employees witnessed how companies furloughed or laid off their colleagues during business slowdowns. Those who remained resented being told to shoulder greater burdens and put in more time (sometimes with suboptimal resources) to help keep operations afloat.

Because they are exhausted. Our research shows that poor mental health (burnout and stress), family-care demands, and reflections on purpose because of the COVID-19 pandemic played big roles in why some workers left their companies without another job in hand. Consider the couple who, after two years of stressful, isolating remote work in their respective jobs, realized they could get by on one income as a trade-off for spending more time with their children. Among those who quit, attrition was most apparent in the consumer and retail, healthcare, and education sectors—industries that have felt some of the greatest social and economic pressures during the pandemic.

Of the almost 600 employees we polled who voluntarily left a job without another in hand, 47 percent returned to the workforce in either traditional or nontraditional work arrangements.

Why are some employees returning?

Because they want to. It’s complicated, but for reasons relating to the state of personal health and finances, outreach from people in their networks, dissatisfaction with start-up experiences, and so on, some employees have started to return to traditional employment. Of the almost 600 employees we polled who voluntarily left a job without another in hand, 47 percent returned to the workforce in either traditional or nontraditional work arrangements. Almost a quarter of the returnees took up nontraditional work, while 76 percent went back to traditional employment. The latter group cited workplace flexibility, adequate compensation, and reasonable expectations about performance as top factors in their decision to return (Exhibit 2). Only 21 percent went back to work in the same sector and assumed roles at a similar level as those they left.

Are they back for good, or just for now?

Our research shows that 25 percent of the employees who voluntarily left and then returned (to both traditional and nontraditional roles) are at least somewhat likely to leave their current employers in the next three to six months. They know that other opportunities are out there—particularly in this strained labor market. And they say that if professional development, workplace flexibility, support for mental and physical health, and other needs aren’t being met at one company, they will look for the right conditions elsewhere (Exhibit 3).

What if you subsidized cleaning services instead of gym memberships? Or what if you invested in on-site childcare services that would allow employees to eat lunch with their children?

How do you bring them back—and keep them?

Companies’ general response to the employee exodus has been to do more of the same—using short-term Band-Aid solutions to address labor shortages. For instance, some big-box retailers are offering to pay store workers daily, rather than weekly or biweekly, to make jobs more appealing. Other companies are paying extra to keep disengaged employees on board, even if productivity is taking a hit, simply because they need workers.

Companies won’t be able to justify and sustain these moves for the long term, however. To start to repair relationships with employees, companies must take a different approach, focused on the following core principles.

Pay to play: Revise compensation and benefits

Business leaders can’t just write one big check after another and expect that to keep employees in the fold. But that’s what many are trying to do. In one financial-services company, for instance, during the pandemic, leaders increased salary ranges by 15 percent to try to keep employees from leaving, but attrition levels stayed the same. That’s because the company had not addressed concerns about untenable hours and high-pressure assignments in the middle of a global pandemic. Nor had it acknowledged the churn going on within the industry.

Companies will need to restructure compensation packages in ways that will attract and retain disillusioned employees. There is no one right way to do this; a lot depends on context, and some trial and error may be involved. Business leaders will need to ask themselves certain questions: What do the market rates look like? Given prevailing rates, does it make sense (for, say, the big-box retailers mentioned earlier) to pay workers daily—or will that just encourage short-term stays and greater attrition? Companies must remember that pay transparency is at an all-time high. If current employees find out that the company is offering higher pay to new hires or otherwise changing pay practices to lure new employees to the company, they may request raises of their own, which could drain the organization of resources needed to fight other fires—possibly prompting even more departures.

As part of their discussions about compensation, companies should also consider which benefits employees would need to find the work–life balance that they say is critical for their return. What if you subsidized cleaning services instead of gym memberships? Or what if you invested in on-site childcare services that would allow employees to eat lunch with their children? Companies must assess standard compensation against the types of relational factors that employees say they want—such as mental-health services or various forms of flex time—and find the right balance.

Play to win: Make your workplace sticky

Compensation and benefits reviews are just the first step; companies must also invest in building “sticky” workplaces—listening to employees, anticipating and addressing their concerns, fostering psychological safety and a sense of community, and measuring outcomes. Rather than conducting only exit interviews, for example, has your company implemented “stay” interviews, asking people in the most critical roles how they are doing and what they need to continue in those roles?

Based on responses, companies might introduce new types of scheduling, staffing, and hiring innovations—for instance, why not establish a midday shift for workers, or allow people to assemble their own teams for projects rather than assigning them to ready-made squads? One retailer has simplified its application process for new candidates, hoping to decrease the time to hire and quickly expand its workforce. Other businesses might want to let job candidates test out roles for a limited period or directly interview potential colleagues in those areas of the company that interest them most.

Over the past two years, some companies have tried other relatively simple sticky compensation-related moves, including offering “well-being” bonuses to employees or providing extra days off for professional development or mental-health breaks. One theme park and entertainment company has offered to pay 100 percent of the tuition costs for employees seeking higher education.3

In this new competition for talent, employers should acknowledge the different roles that compensation can play, as both a hygiene factor and a source of motivation. Individuals may be looking for a certain range of pay when considering a job offer. But once that threshold has been met, cultural factors can make a company more attractive to join and, ideally, provide more incentive to stay. Focusing only on compensation or only on cultural factors won’t stem the tide of attrition. Business leaders must pay constant attention to both.

Stack the deck: Expand your talent pool

In most companies, talent acquisition teams focus on enticing, screening, interviewing, and hiring candidates who fit the traditional definitions of a job applicant. To compete successfully for today’s workforce, however, they must think more creatively about candidates: What about the nontraditional workers who aren’t even on their radars? These might include students, “boomerang” employees—those who return to a company after leaving—and others currently doing part-time or contract work or leading their own one-person start-ups.

Even more important, talent acquisition teams must find ways to attract latent workers—those who are not in the workforce at all, and not actively seeking a traditional job at a traditional employer, but who might return with the right offer and under the right conditions. Maybe they are burned out and on an indefinite break. Maybe they left the workforce during the pandemic to take care of their kids but are considering a return now that schools are getting back to normal schedules. Based on our conservative calculations, this untapped source of labor could be as many as 23 million people.4

It is incumbent upon talent acquisition teams to identify and woo these potential candidates—and to do so quickly. The longer these workers are sidelined, the more training they will need to get back up to speed with certain skills (Exhibit 4).

To reach nontraditional workers, companies must actively lower the barriers to entry and rethink requirements for certain roles. For example, do candidates really need an advanced degree to fill a critical role, or will a certificate of specialization or an apprenticeship suffice? Consider one possible cohort of nontraditional workers: those who have had run-ins with the law. Many states now have “ban the box” policies that require companies to remove any questions about convictions or arrest records from job applications and to delay background checks until later in the hiring process.5 For some companies, this change—along with the existence of organizations such as Homeboy Industries, which provides placement services and support for former gang members looking to reenter the workforce—could help them access nontraditional talent.

To reach latent workers, companies must be willing to change their approaches to hiring. Instead of using the same old online hiring platforms and keeping their searches local, talent acquisition teams should think creatively about their referral programs—for instance, launching a personalized “phone two friends” campaign, asking existing employees to recruit within their networks—and acknowledge that the best candidates may be outside the immediate radius of the company’s headquarters.

Even before doing any outreach, employers should consider the critical skills that the company requires and determine the universe of potential candidates inside and outside the company who possess these skills. Is that universe shrinking or growing—now, and five years from now? How many tasks could be automated? One financial institution performed such an analysis and realized that salespeople were spending the bulk of their days processing orders and managing documents rather than pursuing actual sales.6 With this information in hand, business leaders could redefine and reassign roles in a way that would not only be more meaningful and manageable for overworked employees but also create more value for the company.

The new competition for talent is not just about employers competing with one another to find the best workers; it’s about employers acknowledging the many choices that today’s workers have and finding effective ways to compete against all those options. The old playbooks won’t work. Even for those companies that end up figuring out how to bring some people back, there will be inevitable setbacks (and further waves of attrition) if they can’t figure out how to retain those workers.

By following the principles offered here, however, companies can start to build a true capability in attraction and retention, transform themselves into destination workplaces, and meet the ever-changing needs of this and next-generation workforces.

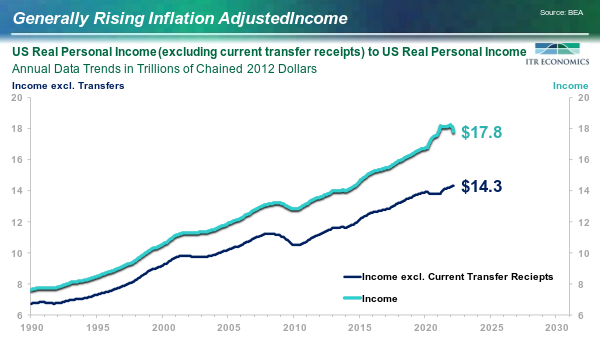

This is either a glass-half-full or glass-half-empty moment as you look at the chart below. How you perceive the trends on the chart likely says a lot about your expectations. You could focus on the upper (thicker) line and see that Personal Income (real means adjusted for inflation) surged during COVID and is now down from that elevated level. The decline in Real Personal Income could be a harbinger of ill tidings for retail sales and therefore the broader economy.

Three factors should be considered if you are going down that road.

The level of Real Personal Income is still well above pre-COVID levels.

The current status of Real Personal Income is essentially on trend relative to the pre-COVID trend.

The surge (and subsequent decline) was caused by the overwhelming amount of stimulus dollars supplied to individuals.

It is likely that the Real Personal Income trend will be sluggish at best in the second quarter as the normalization of transfer payments (beyond the stimulus) becomes the sustaining feature.

The lower trend line is Real Personal Income excluding transfer payments. No stimulus or other government largess is involved in the lower trend (thinner line). The income trend that excludes direct government involvement is positive. Observations on the Real Personal Income trend sans government involvement:

The current value is higher than pre-COVID. Adjusted for inflation, people are generally making more than before the COVID recession.

Point #1 means spending power is generally “up.”

It is important to note that 1Q22 came in virtually flat relative to 4Q21.

A surge in inflation tends to lead wage increase, so the recent flatness is not surprising.

Our forecast suggests that incomes will remain relatively soft in 2Q22 after adjusting for inflation. This likely ties in with the projected deceleration in retail sales (both adjusted for inflation and not adjusted for inflation). Our forecast also projects rising Real Personal Income Excluding Transfer Payments in the second half of 2022 and the first quarter of 2023. Applied to the probability of a lessening of supply chain pressures (alternative sourcing, slowing world growth, empty containers making their way back to Asia, alternative sourcing for neon, etc.), the improvement in inflation-adjusted incomes suggests we are on track for the projected re-acceleration of the US economy post mid-2023.

The ability to effectively lead others is a key to success in growing a business. But in the transactional business world gone virtual, we spend the majority of our time treating one another as strangers.

Taking into account all the digital exchanges we have in the course of a workday, what can we as leaders do to humanize our interactions, draw people to us, and build trust?

It comes down to one word: curiosity.

Research has found that curious people are known for having better relationships, and other people are more easily attracted and feel socially closer to individuals who display curiosity.

Curiosity is a strong foundation for developing a growth mindset so you can keep learning. Research published in Harvard Business Review states that people with a higher curiosity quotient (CQ) are more inquisitive and generate more original ideas, and this thinking style leads to higher levels of knowledge acquisition over time.

Organizations will also benefit greatly from hiring future workers displaying curiosity. In one study published in HBR, “the most curious employees sought the most information from co-workers, and the information helped them in their jobs–for instance, it boosted their creativity in addressing customers’ concerns.”

From a leadership standpoint, by being willing to explore and ask questions with curiosity, you’re able to see more clearly the nuances of a challenge and reach better outcomes.

But here’s the thing. If you’re in a bureaucratic environment, too often bureaucracy or the status quo drives us to stop being curious and asking questions, as we think we already have the answers. But by building your curiosity, and allowing others to do the same, we open ourselves up to new ideas that may solve complex problems at a much faster pace.

Reverse mentoring

To take your curiosity quotient to the next level, reverse-mentoring programs are emerging, as companies realize that top-down learning is not always appropriate.

In reverse mentoring, a junior team member enters into a professional friendship with someone more senior, and they exchange skills, knowledge, and understanding. For example, a younger team member might be more tech savvy, so encouraging a pairing with an older colleague or manager with less experience using technology can improve that manager’s ability to connect with potential customers.

This is not a new idea. In the late 1990s, General Electric asked 500 of their top executives to seek out mentors from among new employees.

Reverse mentoring recognizes that there are skills gaps on both sides, and that each person can address their weaknesses with the help of the other’s strengths. A younger team member can pass up-to-date skills and ideas up the corporate ladder, and someone older can become a mentor or coach to that person.

Bill Gates’s take on curiosity

In 2019, Bill Gates spoke to students, parents, and alumni at his high school alma mater in Seattle. One question posed to Gates is especially noteworthy for the next working generation: “What are the skills today’s students need to know to thrive in the world of 2030 and 2040?”

Gates stressed the critical importance of curiosity as a framework for acquiring knowledge. A growth mindset as the foundation and drive to stay curious and keep learning, said Gates, will help prepare future workers for the immense changes that will take place.

What’s the true failure rate of small businesses? Well, it depends on who you ask and whether it includes pandemic closures or not. Or, if there were economic or political drivers that worsened the closures. And frankly, it depends on who is counting and how they’re counting. It is arguable that the mistakes that make or break small businesses are similar across industries and geography. Whether it’s focusing attention on places that don’t produce income or build relationships, not setting boundaries or ignoring their online reputation, I’ve watched small businesses make these mistakes that make or break them.

Seven mistakes that make or break small businesses

1. Not defining an ideal client

I attended my first networking meeting more than a decade ago. There was a woman who represented a skincare line who said, “My ideal clients include anyone with skin…” While it’s great to be able to serve anyone who comes to you, it is also important to have a specific ideal client well-defined. That doesn’t mean you can’t work with others. It simply focuses your marketing efforts, including your short presentation at a networking meeting. A better commercial would be: My ideal client is a woman of a certain age who is concerned about fine lines and wrinkles. Failing to define an ideal client means your business can go in any direction and you become #2.

2. Busy but not productive

If you don’t know who your ideal client is, you set meetings with anyone in the hopes to find your clients. You become busy but not productive. I can still remember a couple of guys from years ago who ran around to networking meetings like it was their job. And in some sense, I guess it was their job, or at least what their business had become. They just didn’t know who they wanted as an ideal client. So they wasted a lot of time doing activities that were not income-producing. They looked busy but when I sat down with them, they were struggling financially. It was sad to hear but it was also a good lesson. When you focus your efforts, you get more accomplished and business grows.

3. Not setting boundaries

If you like working weekends, late into the night or during a time when you’d otherwise not want to be working, then do not set boundaries. If you want a life outside of business, set boundaries. I’ve found that if I don’t send emails or contact clients when outside of my normal work hours, they respect my time. Boundary setting is also important in contracts or agreements when describing the scope of the project. If a client wants more work, I have a stipulation in the agreement for the cost for work outside the scope of the original project. It saves a lot of time for everyone wondering what is within the scope and what is not. By clearly defining the hours and scope of the project, I can focus on the work and delivery. Without those in place, I could be working on a project indefinitely.

4. Ignoring reputation management

My husband and I make it our goal to leave positive reviews as much as possible and appropriate. All too often businesses only receive negative reviews, and they deserve positive reviews as well. Whatever review your business receives, you’ve got to be aware of your brand reputation online and respond to all reviews. There are reputation management companies whose sole focus is to respond to reviews, both good and bad. It can be a great investment for your business to hire one of them.

5. Working without a contract

Find out what your state requires to be considered a contract. An email of terms that each agrees to within the email that is dated is sufficient in some states while others may require an official, wet signature contract. Not only does the contract define the cost and payment terms, but it should also define the scope of the project. That means if the client wants more work, there is an added cost. Allow for a provision for work that is out of scope that will be billed at an hourly rate or whatever is customary in your industry. This will save you from miscommunication when you have a contract in which to refer. When the client asks why you can’t do additional work, tell them it’s out of scope per the terms of the agreement and what the cost is if they’d still like the work completed.

6. Not selecting a business structure

What I mean by this is that you haven’t incorporated or created an LLC for your business. Without one of these, you’re operating as a sole proprietor and personal assets are all at risk should the business be sued or sent to collections. Once a business structure is selected and set up, put an Operating Agreement (LLC) or Bylaws (Corporation) in place. You need to do this so that in the event you are incapacitated or worse, your business can continue without you. That means employees and vendors get paid, along with other receivables. Clients can continue receiving goods and services. Your family will also be protected.

7. Not collecting outstanding invoices

I can’t tell you how many freelancers post in social media groups that they are having trouble collecting from a client. And, they continue to do work for the client! I have a stipulation in my agreement that if invoices aren’t paid within a certain number of days, the work stops until the account is made current. You can also keep credit cards on file or set up a monthly subscription, so you’re paid automatically. In 11-plus years of freelancing, I’ve had one $75 invoice left unpaid. The rest are paid, and most are paid on time. Make it part of your contract and process for clients to pay you on time.

Without processes and boundaries, small businesses can easily work many hours with little to show for it on the bottom line. Learn from others the right ways to do business. Avoid these mistakes and be productive. Success is yours to be had!